10th October 2025

Publication Information

Download Publication

- 497 KB PDF

- 10th October 2025

Stay Informed

Get email updates about new ACCR research and shareholder advocacy on specific topics of interest to you.

Sign UpThis communication is for informational purposes only and does not constitute financial, legal, or professional advice. ACCR does not hold an Australian Financial Services Licence and does not provide financial product advice. The purpose of this communication is not to provide financial product advice. Please read the terms and conditions attached to the use of this site.

The Australasian Centre for Corporate Responsibility (ACCR) is pleased to participate in the Inquiry into the role of Western Australia in the global effort on decarbonisation.

ACCR is a philanthropically-funded, not-for-profit, research and shareholder advocacy organisation, focused on the investment risks and opportunities brought about by the global energy transition. We closely monitor how climate-related risks are being managed by a selection of heavy-emitting companies, and we enable institutional investors to engage effectively with these companies.

Our response to this inquiry is focused on the following points:

The pathways our major trading partners have to decarbonising and the potential for Western Australia to contribute through: a) LNG exports, to provide energy security as they exit coal and transition to renewable energy.

WA's LNG does not have significant potential to enhance the decarbonisation or energy security of Australia's trading partners, because decarbonisation is driven by renewables.

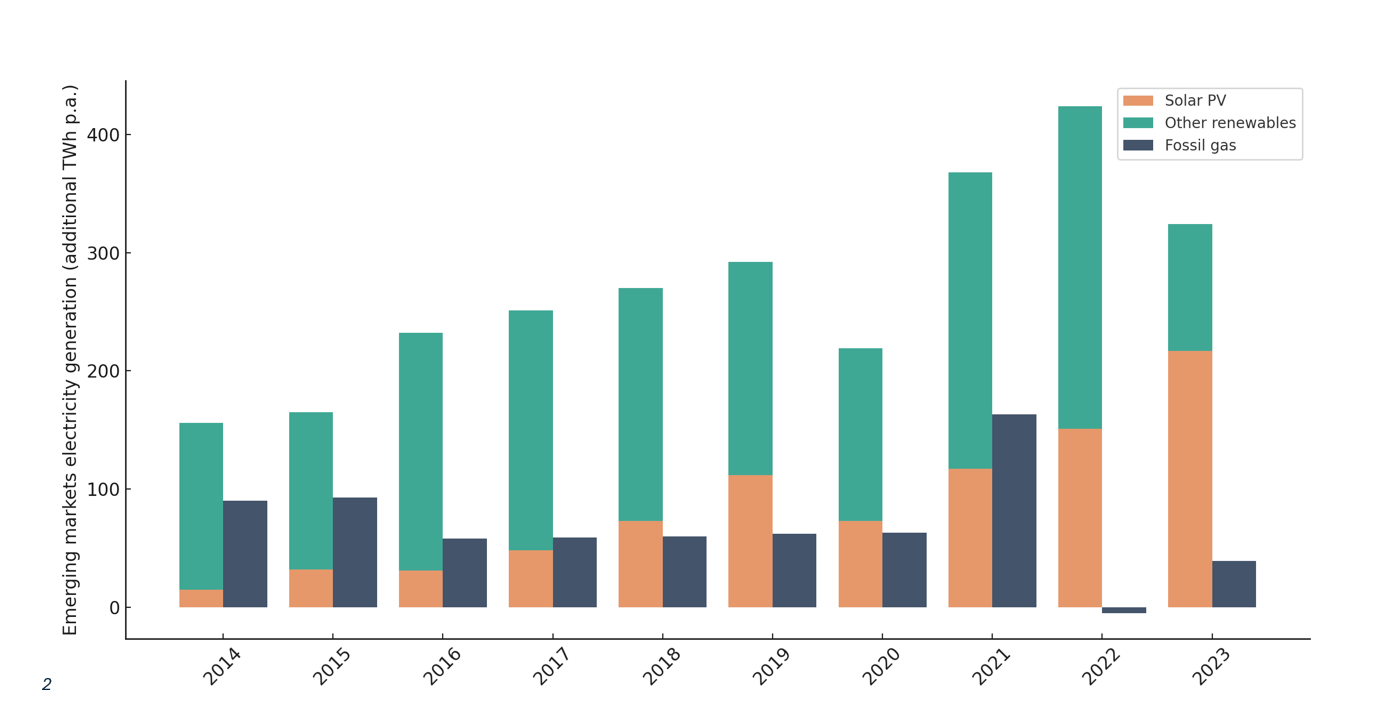

Renewables are capturing an increasing share of the energy market. This is because they are cheaper, cleaner and faster to deploy than LNG. Renewables also reduce reliance on imports, improving domestic energy security in times of geopolitical uncertainty.[1]

Figure 1: Renewables are growing 8x faster than gas generation in emerging markets[2]

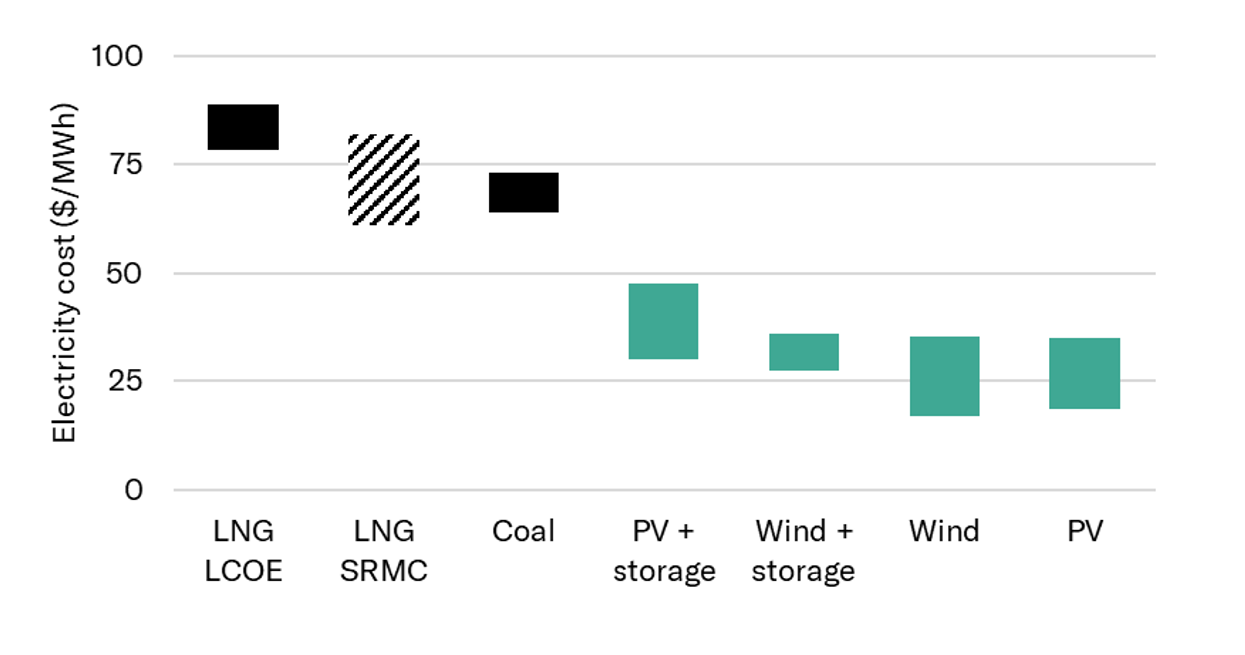

For LNG to compete with renewable electricity, LNG prices would need to drop by more than 50%, to below US$5/MBtu. This is below the cost of production for most of the world's LNG supply, including Western Australia's latest LNG project Scarborough/Pluto 2, which cost ~US$6.50/MBtu.[3]

Figure 2: LNG is not a cost competitive electricity source in China[4]

Emerging markets are highly price sensitive. Many are already leapfrogging LNG, due to the cost advantages of renewables and the added energy security that locally produced renewables provide. For example, in the first six months of 2024 Pakistan imported 13GW of solar panels.[5] It is now delaying and redirecting its contracted LNG cargoes.[6] These changes are materially eroding projected fossil fuel demand. Since 2021, the International Energy Agency's projections for solar capacity have more than tripled, whilst projections of gas growth have decreased by 120% (and 90% for oil).[7]

Some LNG importing countries are reducing their reliance on LNG. Japan's latest Strategic Energy Plan seeks to reduce reliance on imported thermal power in favour of domestic nuclear and renewable energy.[8] Japan is increasingly reselling its LNG imports, contrary to its claims it needs the fuel for energy security,[9] while its efforts to create LNG demand in emerging Asian markets by investing along the value chain are yet to bear fruit and continue to face considerable uncertainty. Japan's financing of the LNG value chain has not generated significantly more demand in emerging Asian markets, with most of the LNG Japan resells still going to existing, mature markets.[10]

Claims by the LNG sector that it can contribute to the decarbonisation of our major trading partners should be carefully scrutinised.

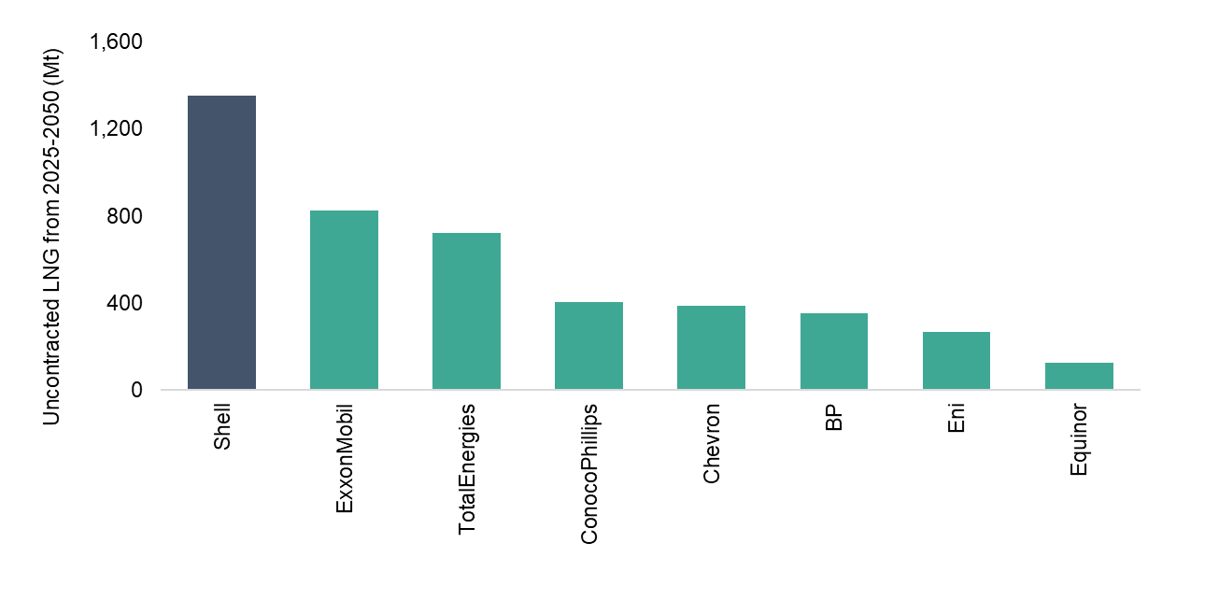

LNG producers - including in Western Australia - have a multi-billion dollar incentive to exaggerate the future role of LNG, due to their large, uncontracted LNG portfolios.

Shell, for example, has more than 1 billion tonnes of uncontracted LNG that it needs to sell before 2050, which is worth over US$500 billion at current prices.

Woodside, BP and Chevron each have 400 Mt of uncontracted LNG to sell before 2050.

Figure 3: Shell has over 1.4 billion tonnes of uncontracted LNG between 2025 and 2050[11]

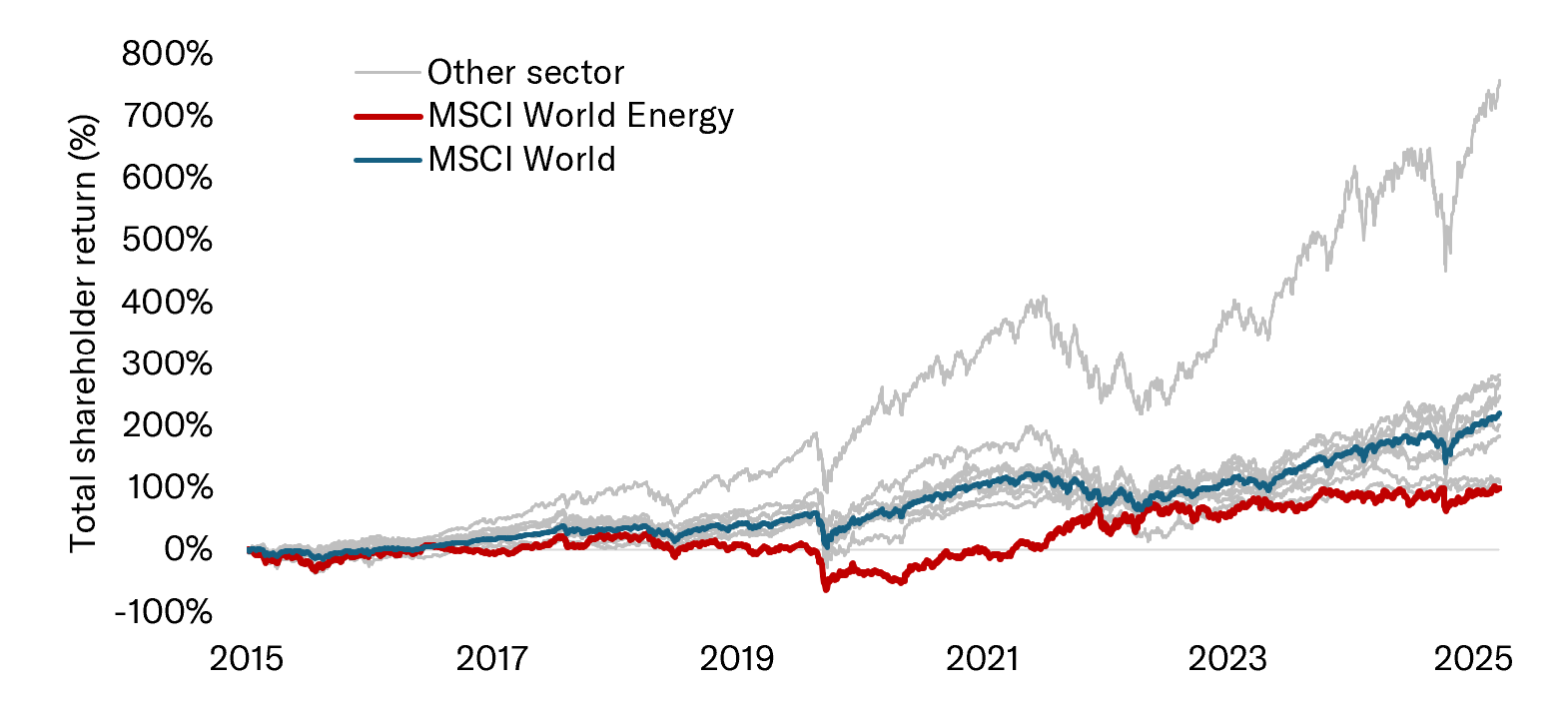

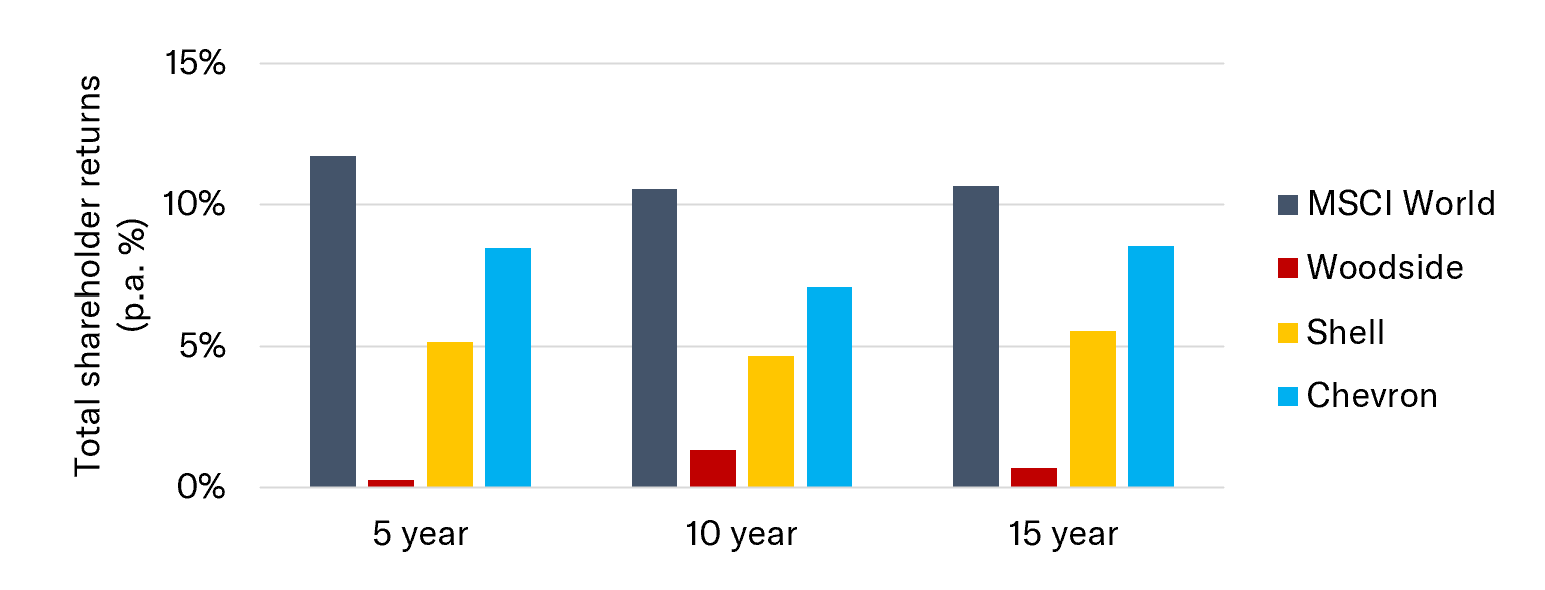

The reality for the oil and gas sector is that it is a chronic underperformer - it has delivered lower shareholder returns than every other sector on the MSCI over the last decade - and it faces an even more challenging future as policy and clean technology continue to place downward pressure on oil and gas demand.

Figure 4: The oil and gas sector has delivered lower shareholder returns than every other sector over the last decade[12]

Figure 5: Woodside, Shell and Chevron have all underperformed the global share market[13]

The LNG industry's claims that LNG will help improve energy security and enable decarbonisation in Asia have come under question. For example, Woodside's claim, including in official regulatory applications, that gas produced from the Scarborough project would reduce global emissions by replacing thermal coal in Asian markets. It made this claim even after research it commissioned CSIRO to undertake in 2019 found that without a global carbon price, more Australian LNG exports would increase emissions in Asia, prolong coal use and displace renewables.[14]

ACCR has refuted similar claims in previous analysis, outlining how Australian LNG was not materially displacing coal in Asia because it was too expensive, even for short duration firming of renewables.[15] Whilst there have been examples of (non-liquefied) gas displacing coal, such as in the US, this has occurred where gas is cheap and domestically produced. LNG is neither cheap nor domestically produced.

The think tank InfluenceMap has also refuted claims made by the LNG industry in consultation submissions to the Future Gas Strategy, that new Australian fossil fuel supply is required to support the decarbonisation of Australia's trading partners.[16]

In June 2025, the Asia Natural Gas & Energy Association (ANGEA), a LNG lobby group, published research it commissioned from S&P Global. ANGEA and its member company Woodside claimed the study showed that replacing coal with a "balanced" mix of LNG and renewables would reduce emissions in Asia. However, the study did not include scenarios that could reduce emissions by a greater amount by displacing both coal and most gas with renewables. This type of scenario could have been both cheaper and lower emissions - highlighting that increased LNG is not an effective way to decarbonise the region.

It avoided discussing this type of scenario by constructing its own lower emissions scenario that assumed variable renewables would be firmed with 20% hydrogen, which is implausible. Hydrogen is unlikely to form a meaningful part of the electricity system, let alone 20%, with CSIRO finding that hydrogen generated electricity is four times the cost of firmed, 90% variable renewable electricity.[17]

The pathways our major trading partners have to decarbonising and the potential for Western Australia to contribute through: c) Green iron

Western Australia has a significant opportunity to enable decarbonisation through the creation of green iron hubs.

WA is the world's largest exporter of iron ore, producing ~99% of Australia's iron ore exports and meeting 58% of global import demand.[18] With its exceptional solar and wind resources, WA has an opportunity to co-locate renewable generation, hydrogen production, and iron ore beneficiation to create globally competitive green iron hubs. Analysis by the Chamber of Minerals and Energy Western Australia in collaboration with Mandala suggests that WA could supply more than 14% of global green iron by 2050, reducing global emissions by 456 MtCO2 annually[19] - equivalent to almost Australia's entire domestic emissions.

ACCR's multi-year engagement with investors in iron ore and steel companies across Europe, Asia and Australia informs our view that investors are:

Global investors are increasingly recognising that the decarbonisation of steel supply chains is essential to managing long-term financial risk. Steelmaking contributes 7-9% of global greenhouse gas emissions, with ~90% arising from coal-based blast furnaces.[20] In 2021, Agora Industry projected that more than 70% of existing coal-fired blast furnaces globally would require reinvestment decisions by 2030.[21] Whether these are relined with coal or replaced with genuinely green technologies will determine the sector's emissions trajectory for decades.

ACCR's 2024 global investor survey of 500 respondents across 34 countries found:[22]

Many reputable organisations have produced strong economic and industrial analyses of WA's green iron opportunities:

Despite these advantages, Australian iron ore majors remain under-invested in green iron.

Investors increasingly view such allocations as insufficient compared to earnings and inconsistent with credible Paris-aligned pathways. There is growing investor frustration with this mismatch, with many investors signalling a willingness to escalate through voting, shareholder resolutions, and capital reallocation.

ACCR recommends the following actions for the WA Government to seize green iron opportunities:

WA has a once-in-a-generation opportunity to pivot from exporting raw ore to exporting green iron. If realised, this would cut the equivalent of nearly Australia's entire annual emissions, add billions in export value, and position WA as a cornerstone of global steel decarbonisation.

ACCR, 2025, Investor Briefing: Shell's gamble on gas, 2025, slides 17-18 and 24. US$5/MBtu is determined based on adjusting the gas price in BloombergNEF's LCOE model, assuming a 50% gas generator efficiency. ↩︎

ACCR, 2025. Analysis presented in Investor Briefing: Shell's gamble on gas, https://www.accr.org.au/research/investor-briefing-shell’s-gamble-on-gas/, slide 24. Analysis uses IEA, WEO 2024 data, interpolated using CAGRs where raw data was not available. ↩︎

Woodside, Scarborough FID Teleconference and Investor Presentation, 2021, p4. We adjusted the quoted US$5.8/MBtu for inflation, to reach US$6.50. ↩︎

ACCR, 2025, Investor Briefing: Shell's gamble on gas, https://www.accr.org.au/research/investor-briefing-shell’s-gamble-on-gas/, slide 25. ↩︎

Bloomberg, August 2024, 'Pakistan Sees Solar Boom as Chinese Imports Surge, BNEF Says', https://www.bloomberg.com/news/articles/2024-08-09/pakistan-sees-solar-boom-as-chinese-imports-surge-bnef-says. ↩︎

Pakistan Today, January 2025, 'SNGPL seeks PLL's intervention to address surplus RLNG cargoes for 2025', https://profit.pakistantoday.com.pk/2025/01/25/sngpl-seeks-plls-intervention-to-address-surplus-rlng-cargoes-for-2025/#:~:text=Pakistan imports 10 LNG cargoes monthly%2C with nine,sector unable to fully utilise its allocated LNG. ↩︎

Refers to the change in demand between 2025 and 2050 in the IEA's Stated Energy Policy Scenarios. ↩︎

ACCR, February 2025, 'Investor Bulletin: What Japan's new Strategic Energy Plan means for J-POWER', https://www.accr.org.au/insights/investor-bulletin-what-japan’s-new-strategic-energy-plan-means-for-j-power/. ↩︎

IEEFA, May 2025, 'Churn and earn: How Japan cashes in on resales of Australian LNG at local gas users' expense', https://ieefa.org/articles/churn-and-earn-how-japan-cashes-resales-australian-lng-local-gas-users-expense. ↩︎

IEEFA, 2024, Japan's LNG resales into overseas markets hit record high in FY2023 as domestic demand plummeted, https://ieefa.org/resources/japans-lng-resales-overseas-markets-hit-record-high-fy2023-domestic-demand-plummeted; IEEFA, 2025, How Japan cashes in on resales of Australian LNG at the expense of Australian gas users, https://ieefa.org/resources/how-japan-cashes-resales-australian-lng-expense-australian-gas-users. ↩︎

ACCR, 2025, Investor Briefing: Shell's gamble on gas, https://www.accr.org.au/research/investor-briefing-shell’s-gamble-on-gas/, slide 9, ACCR analysis of Rystad Energy Data. ↩︎

ACCR analysis of Bloomberg data. TSR calculated on a USD basis for 10 years ending 30 June 2025. ↩︎

ACCR analysis of Bloomberg data. TSR calculated on a USD basis for periods ending 30 June 2025. ↩︎

Grieve, 2022, Woodside contradicts CSIRO report debunking key climate claims, https://www.smh.com.au/business/banking-and-finance/woodside-contradicts-csiro-report-debunking-key-climate-claims-20220307-p5a2d5.html ↩︎

ACCR, 2022, 'Facts Over Fiction: Debunking Gas Industry Spin', https://www.accr.org.au/research/facts-over-fiction-debunking-gas-industry-spin/ ↩︎

InfluenceMap, 2024, Australia's Future Gas Strategy: Corporate Advocacy and Industry Narratives, https://influencemap.org/briefing/Australia-Future-Gas-Strategy-26628#briefing_section-26658 ↩︎

CSIRO (Graham, Hayward and Foster), 2024, GenCost 2024-2025, p. 76, https://www.csiro.au/-/media/Energy/GenCost/GenCost-2024-25-Final_20250728.pdf ↩︎

Mandala & Chamber of Minerals and Energy Western Australia, Realising WA's green iron potential, 2024, https://mandalapartners.com/reports/realising-wa-green-iron-potential ↩︎

Mandala & Chamber of Minerals and Energy Western Australia, 2024, Realising WA's green iron potential, https://mandalapartners.com/reports/realising-wa-green-iron-potential ↩︎

International Energy Agency, 2020, Iron and Steel Technology Roadmap, https://www.iea.org/reports/iron-and-steel-technology-roadmap; ACCR, 2024, Forging pathways: insights for the green steel transformation, https://www.accr.org.au/research/forging-pathways-insights-for-the-green-steel-transformation/ ↩︎

Agora Industry, 2021, Global Steel at a Crossroads, p.3, https://www.agora-energiewende.org/fileadmin/Projekte/2021/2021-06_IND_INT_GlobalSteel/A-EW_236_Global-Steel-at-a-Crossroads_WEB_V2.pdf ↩︎

ACCR, 2024, Ahead of the game: investor sentiment on steel decarbonisation, https://www.accr.org.au/research/ahead-of-the-game-investor-sentiment-on-steel-decarbonisation/ ↩︎

Climate Energy Finance, 2024, Green Metal Statecraft: Forging Australia's green iron industry, https://climateenergyfinance.org/wp-content/uploads/2024/11/CEF_Green-Metal-Statecraft_FINAL.pdf ↩︎

Mandala & Chamber of Minerals and Energy Western Australia, 2024, Realising WA's green iron potential, https://mandalapartners.com/reports/realising-wa-green-iron-potential ↩︎

The Superpower Institute, 2024, A Green Iron Plan for Australia: Securing prosperity in a decarbonising world, https://www.superpowerinstitute.com.au/work/green-iron-plan ↩︎

Business News (Tom Zaunmayr), September 2025, Mid West green iron project signs offtake deal with Thyssenkrupp, https://www.businessnews.com.au/article/Mid-West-green-iron-project-signs-offtake-deal-with-Thyssenkrupp\ ↩︎

BHP, 2024, BHP's Climate Transition Action Plan (CTAP), https://www.bhp.com/sustainability/climate-change/climate-transition-action-plan; see also, ACCR, 2024, Analysis: BHP's 2024 Climate Transition Action Plan, https://www.accr.org.au/research/analysis-bhps-2024-climate-transition-action-plan/. ↩︎

Rio Tinto, 2025 Climate Action Plan, https://www.riotinto.com/en/sustainability/climate-change; see also, ACCR, 2025, Analysis: Rio Tinto's 2025 Climate Action Plan, https://www.accr.org.au/research/analysis-rio-tintos-2025-climate-action-plan-cap/ ↩︎

Get email updates about new ACCR research and shareholder advocacy on specific topics of interest to you.

Sign Up