26th March 2026

Stay Informed

Get email updates about new ACCR research and shareholder advocacy on specific topics of interest to you.

Sign UpThis communication is for informational purposes only and does not constitute financial, legal, or professional advice. ACCR does not hold an Australian Financial Services Licence and does not provide financial product advice. The purpose of this communication is not to provide financial product advice. Please read the terms and conditions attached to the use of this site.

This is an excerpt from our March newsletter. Subscribe to receive our latest research, insights and updates directly to your inbox.

Over the past quarter, we have seen several narratives gaining traction in energy and financial markets. In periods of geopolitical tension, concerns about short-term supply risks can quickly dominate the discussion. However, investors should be cautious about companies extrapolating short-term supply constraints and the associated price spike into long-term capital allocation decisions. This approach is risky, particularly when the underlying economics of the oil and gas sector are deteriorating.

In this edition, we highlight three issues we think investors should pay close attention to:

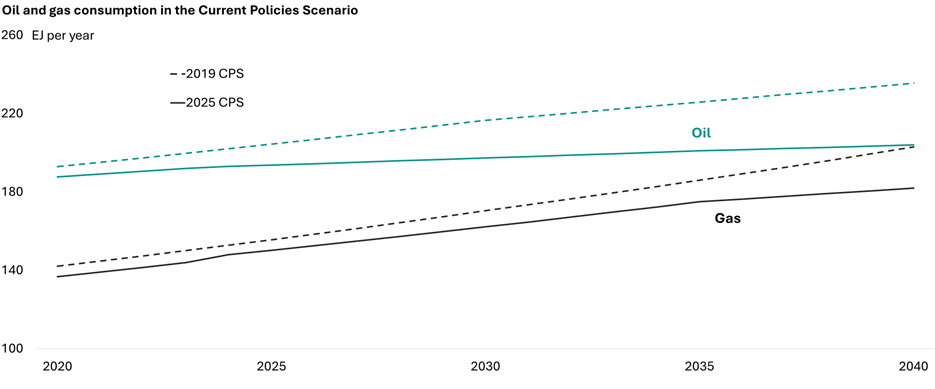

In an ACCR review of the 2025 IEA World Energy Outlook (WEO), we explained why the resurrected Current Policies Scenario (CPS) should not be treated as an investment signal. Similarly, the IEA warns in the WEO that it is “not a forecast or a prediction of how the energy system will unfold” and it should not “be interpreted as a “business-as-usual" scenario”.

Comparing the CPS from 2019 to 2025 shows that the energy transition has been faster than the 2019 CPS envisioned. Oil and gas consumption is lower today than projected in 2019, and the 2025 CPS tracks further below the 2019 version as the scenarios approach 2040.

However, we are now seeing evidence of the oil and gas and financial industries pivoting back to bullish long-term demand scenarios. Recent media commentary suggests investors are now pushing for oil and gas companies to fire up the exploration engine and start growing again, to close a supposed resource gap.

Figure 1: Current oil and gas consumption is below 2019 projections, with the 2025 CPS diverging even further below the 2019 pathway towards 2040. Source: ACCR analysis of IEA data.

This perception is fuelling renewed interest in exploration. However, there are concerns about whether this is in shareholders’ interests, irrespective of whether a resource or future production gap exists. ACCR’s report on ten major oil and gas companies found that since 2000, every dollar spent on conventional exploration has eroded 71 cents on a discounted basis.

It’s clear why exploration is destroying value:

Exploration is clearly a key driver of the sector’s chronic underperformance. However, we’re yet to see an oil and gas company articulate this challenge to investors, let alone develop a compelling strategy to address it. It is also unclear how exploration could increase value, given the rapid shift to renewable energy is eroding the long-term addressable market for oil and gas.

Despite recent geopolitical events causing short-term price spikes, oil and gas assets often have multi-decade cash flows, so investment decisions should be based on market fundamentals rather than today's prices. In our view, oil and gas companies should prioritise shareholder returns over organic growth. But this is not what we’re seeing.

Integrated oil companies are cutting back on shareholder distributions in favour of growth and protecting the upstream budget. BP recently cut its buybacks completely, while Total and Equinor also reduced their buybacks.

Our analysis shows that shareholder distributions may be a more effective use of capital given the poor returns associated with conventional upstream exploration and development and the failed attempts to transition to integrated energy companies. Prioritising questionable exploration and organic growth over shareholder returns is an area that we think engagement teams should be laser-focused on.

Dr Sophie Lewis, ACCR Chief Scientist - Engagement

Is extreme heat relevant to investors? All we have to do is look at data centres to see an escalating problem.

One of the most robust findings from climate science is that any increase in global temperatures will increase the intensity of extreme heat.

As heatwaves become hotter, longer and more frequent, investors face an important question: are these events manageable through adaptation, or do they represent a material financial risk?

The science is clear. There are direct and growing financial impacts from the rise in extreme heat that require investor attention.

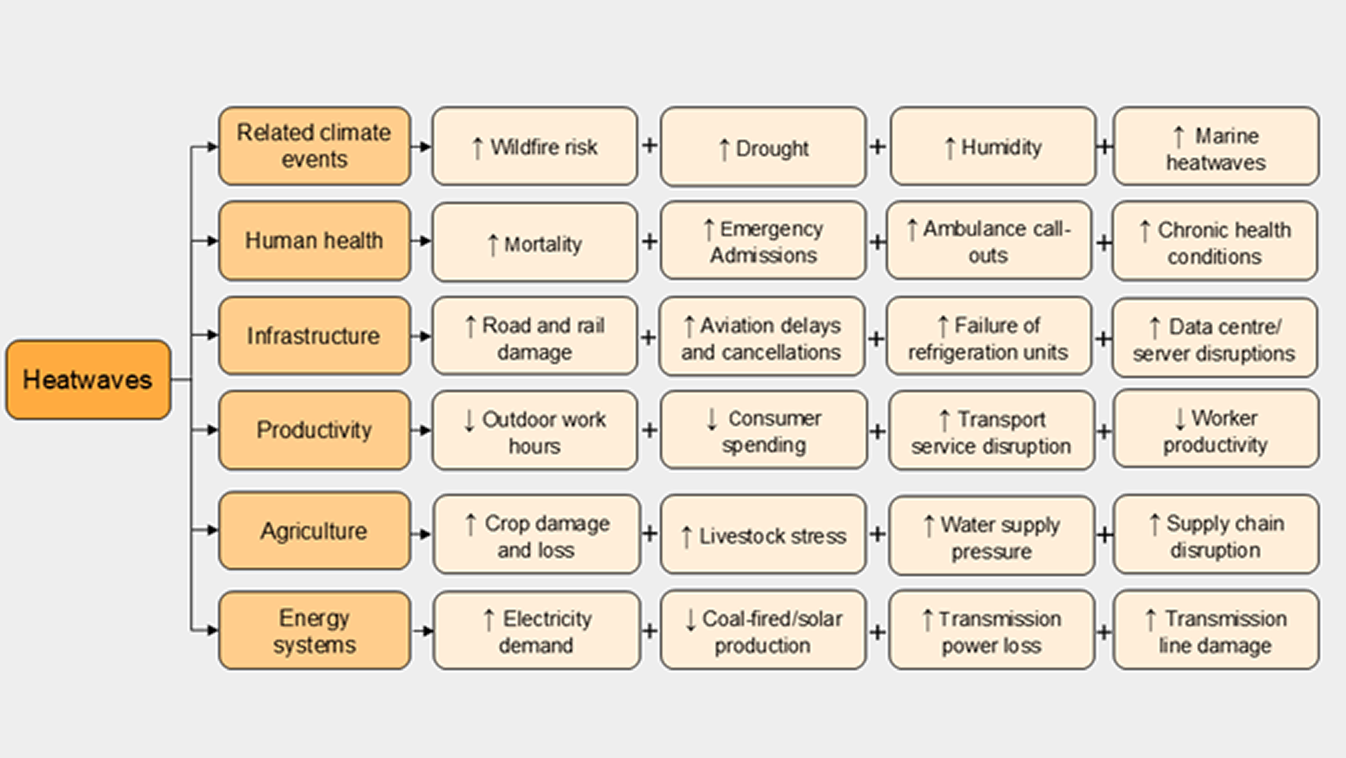

Globally, extreme heat is an underappreciated risk. Heatwaves don’t leave a trail of destruction like wildfires, storms or floods, or lead to rapid damage estimates. However, they can have huge, far-reaching effects that flow through economies, as shown in the chart below.

Figure 2: Heatwaves have extensive impacts that are underappreciated compared to other forms of extreme weather. Source: ACCR.

A growing body of research is demonstrating the increasingly costly impacts. For example:

Data centres are emerging as acutely vulnerable to extreme heat. In 2022, when a heatwave pushed temperatures above 40ºC in London for the first time on record, data centres used by Google and Oracle suffered outages after their cooling systems failed. Later that year, a data centre for the social media platform X in California experienced a similar closure.

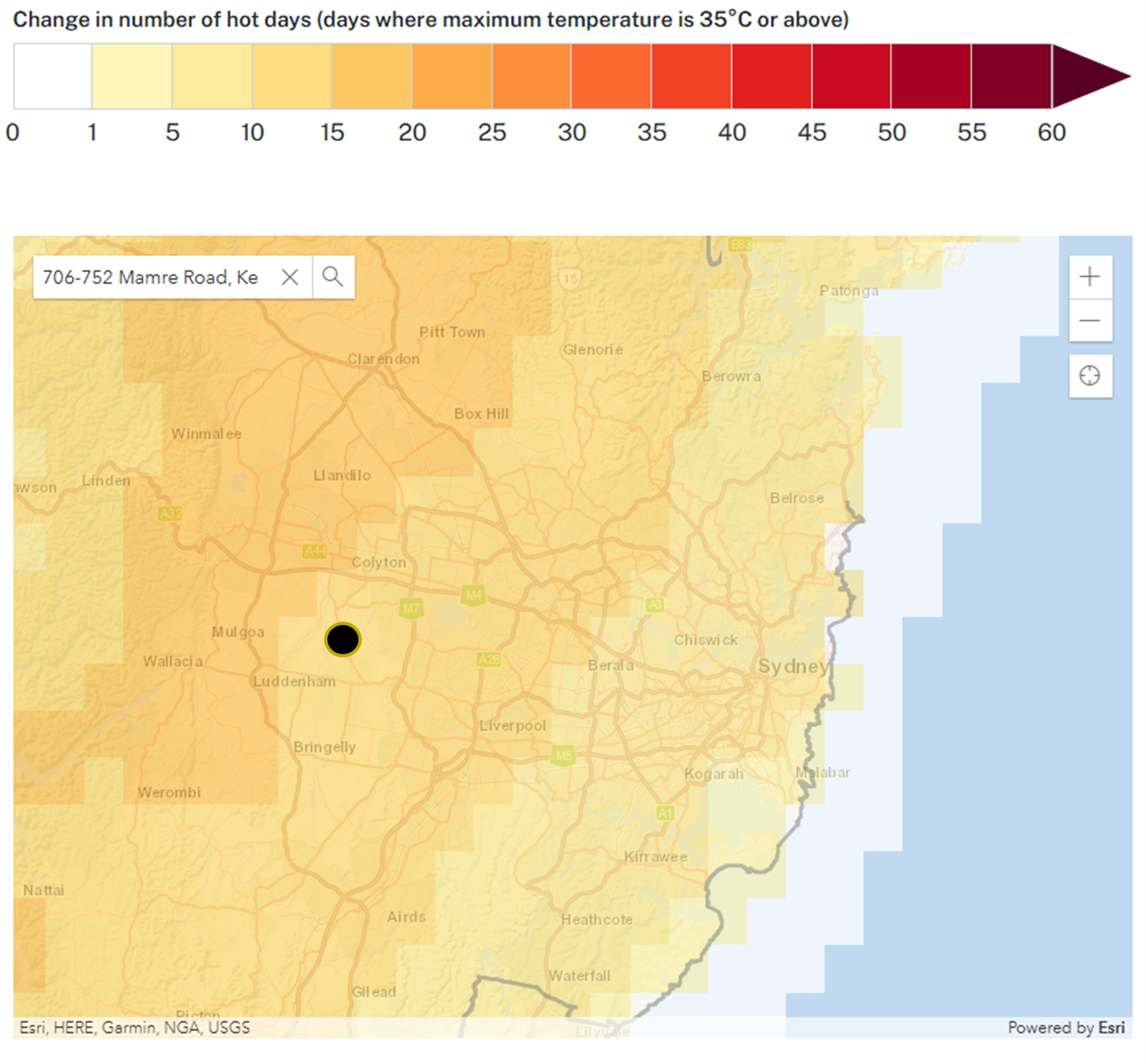

In Sydney, there are more than 90 data centres operating and another 20 under assessment for development. The 1GW Mamre Road Data Centre would be Australia’s largest and is planned to be built just north of Western Sydney Airport. The site is projected to experience 7 to 15 more days above 35°C by 2050, depending on the emissions scenario, which will present an extraordinary challenge to operations. A wave of data centres coming online around the world will face similar risks as temperatures rise.

Figure 3: Projections for increases in hot days in Sydney for 2050s with proposed location of the Mamre Road data centre marked. Source: NSW Climate Data Portal.

Clearly, heat should not be dismissed or considered inconsequential. Rising heat extremes – and their wide-ranging impacts, from data centre closures to lost labour hours – should be a top consideration of investors when assessing physical climate impacts.

Dr. Dimitri Lafleur - Chief Scientist, Insights

Why do physical risk metrics diverge sharply across models? And are they all understating risk?

Investors increasingly rely on climate risk models to report and estimate how future warming could affect assets and portfolios. But the results from different models often diverge significantly and can produce very different estimates for the same portfolio.

Climate risk assessments are produced through a sequence of linked models that connect future emissions pathways to estimates of economic damage. At each stage of this modelling chain, assumptions must be made about how the system behaves, and what inputs are used. When those assumptions and inputs differ, the final estimates can diverge substantially.

Typically, these assessments draw on models across physical, social and economic domains, including:

The Global Association of Risk Professionals (GARP) has highlighted that uncertainties, assumptions and unknowns multiply across each stage of this modelling chain. When models are applied sequentially – linking emissions scenarios through to estimates of economic loss – these uncertainties compound and can lead to widely divergent outputs for the same asset. This is what GARP describes as a “complexity cascade”.

Major sources of divergence include:

For investors, this creates a governance challenge. Climate risk models are highly complex and it is rarely feasible for financial institutions to independently rebuild or fully validate every component.

Instead, investors should seek greater transparency from model providers to develop their understanding of assumptions, limitations and methodologies. This will enable investors to conduct due diligence on physical risk assessments provided by the providers. Investors should expect model vendors to: