The updated IEA Net Zero Emissions (NZE) roadmap shows solar and EVs doing the heavy lifting for 1.5°C

Despite facing challenges, the feasibility of achieving NZE by 2050 remains. This optimism is underpinned by substantial advancements in Solar Photovoltaic (PV) and Electric Vehicle (EV) technologies, coupled with the ongoing enhancement of government climate policies worldwide.

The latest IEA Net Zero Emission report provides an update on the seminal 2021 NZE report. Over the intervening two years, the world has witnessed a global energy crisis and alarming climatic events. 2023 may be the hottest year ever recorded, whilst fossil fuel investment and emissions continue. This is not the path laid out two years ago, but a narrow path remains to achieve net zero emissions by 2050.

Key insights from the IEA NZE 2023 Roadmap:

- Even with no increase in climate ambition, all fossil fuels—coal, oil, and natural gas—will peak before 2030. Although energy consumption will continue to grow, the IEA no longer publishes any scenario where global use of any fossil fuel grows beyond 2030.

- Solar PV, EVs and batteries have met or exceeded the requirements from the 2021 NZE and now play a larger role reaching NZE by 2050. Other technologies like wind and CCS that are not being deployed rapidly enough, play a smaller role.

- Fossil fuel projects that have been sanctioned since 2021 result in higher emissions in 2030, relative to the 2021 roadmap, requiring faster declines between 2030 and 2050. Meeting this faster decline will mean some high cost projects cease production before the end of what would otherwise be their economic lives.

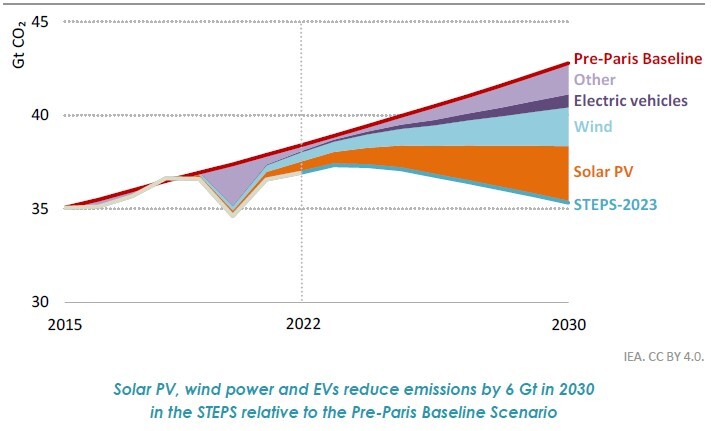

Climate policies continue to tighten, although more action is required to meet a 1.5°C outcome

- Since 2015 the business as usual emissions forecast for 2030 has dropped by 7.5 GtCO2e, largely due to renewables and EVs.

IEA, Net Zero Roadmap: A Global Pathway to Keep the 1.5°C Goal in Reach, 2023 Update, Fig 1.3

- A gradual tightening of climate policies is a design feature of the Paris Agreement’s ‘pledge and review’ mechanism. Although progress will not be linear, forecast emissions are likely to continue decreasing.

- Based on current policies and technology trends, however, emissions are not on track to be aligned with the NZE. They will be 9 GtCO2e above the 2030 target.

Some technologies, including Solar PV and EV are tracking in-line with NZE, keeping the door to 1.5°C open

- The NZE relies heavily on Solar PV and EVs, as they are set to provide around one-third of the necessary emission cuts by 2030.

- Solar energy is now the king of electricity markets and has exceeded its trajectory from the 2021 NZE. PV capacity expanded 40% in 2022 and already announced manufacturing capacity is sufficient to meet 2030 PV production targets.

- EVs have grown explosively, increasing from 4% to 20% of new car sales in just two years. Already announced battery production capacity is almost sufficient to meet 2030 demand from EVs and stationary energy storage.

- The success of PV and EVs has seen these technologies do more of the heavy lifting for emission reductions to 2030.

- Transmission networks are (perhaps somewhat surprisingly, considering the Australian challenges) already expanding at close to the pace required to 2030; with 1.9 million kms pa of new transmission being built globally in the last 5 years; which is 91% of the 2 million kms pa required until 2030 for the NZE.

Other technologies are however lagging

- Technologies, including wind, CCS and hydrogen derived from fossil fuels have not met the targets from the 2021 roadmap and their trajectories in the 2023 roadmap have become less ambitious.

- This has seen their role in the 2023 NZE decline, with reliance on CCS, for example, reducing by 39% in 2030 and 20% in 2050.

Capital and technology are making positive progress

- $1.8 trillion was spent on clean energy in 2022, exceeding the amount spent on fossil fuels by 80%. Significantly more capital is required, but continuing the compound growth in clean energy capex of the last two years is sufficient to meet the clean energy capital target of $4.5 trillion in 2030.

- Technologies are maturing, with 65% of emissions reduction in 2050 now being delivered by technologies that are already commercially available. This is an increase from 50% in 2021.

The role of fossil fuels in the 2023 NZE

- There was no need for new fossil fuel projects in the 2021 NZE, but additional projects have been sanctioned. This causes higher emissions in 2030 and requires faster emission declines after that. Some high cost projects will need to cease production before the end of what would otherwise be their economic lives.

- Coal and oil account for a higher share of energy supply in 2030, attributed to a strong rebound in energy demand post-Covid-19 and a deliberate approach to allow emerging markets more time for clean energy transition.

- Natural gas, however, sees a smaller role, being 10% lower in 2030 and 45% lower in 2050 compared to the 2021 roadmap. This has been driven by price spikes in 2022 and energy security concerns caused by the Ukraine war, damaging its perception as a reliable and affordable fuel.

- The IEA also modelled a delayed action scenario - which sees more short term fossil fuel use. Even in this scenario, there is no need for additional oil and gas use. This scenario sees additional ‘overshoot’ above 1.5°C increasing physical climate impacts. Removing the additional CO2 from the atmosphere in the second half of the century will cost more each year than we currently spend on oil and gas capex and require a land area larger than Peru.

It’s not 1.5°C target or bust

- The path to achieve 1.5°C is still possible, but is now narrow and difficult. If the 1.5°C target is missed however, emissions intensive sectors will still be exposed to transition risk, and sectors exposed to physical climate risks will face greater impacts.

- As mentioned above, the IEA no longer publishes a scenario that sees fossil fuel growth beyond 2030. Fossil fuels are entering terminal decline, the only question is how fast.

- Every incremental temperature increase beyond the 1.5°C target increases physical climate impacts and costs.

The IEA was established to support energy security and its energy scenarios are broadly recognised as the gold standard

- The IEA's updated NZE Roadmap factors in recent global issues such as the carbon-intensive economic recovery from Covid, the energy crisis triggered by Russia’s invasion of Ukraine, and advances in key clean energy technologies like PV and EVs.

- The IEA's NZE pathway incorporates all aspects of its mandate, taking into account energy security, equity, and a just transition for all. It addresses the distinct needs of both emerging and advanced economies in the global energy dialogue, emphasising that countries with energy access issues must resolve these as part of their journey to Net Zero.

Download IEA NZE 2023 Update | 29/09/23

Please read the terms and conditions attached to the use of this site.