16th March 2026

Publication Information

Download Publication

- 707 KB PDF

- 16th March 2026

Stay Informed

Get email updates about new ACCR research and shareholder advocacy on specific topics of interest to you.

Sign UpThis communication is for informational purposes only and does not constitute financial, legal, or professional advice. ACCR does not hold an Australian Financial Services Licence and does not provide financial product advice. The purpose of this communication is not to provide financial product advice. Please read the terms and conditions attached to the use of this site.

ACCR has reviewed BP’s response[1] to the co-filed shareholder proposal[2] (“Resolution 24”). In our view, the response does not provide adequate information for investors seeking enhanced disclosure on upstream capital allocation. BP has recommended that shareholders vote against Resolution 24.

The resolution was filed in response to investor concerns about BP’s long-term performance and the company’s plans to increase spending on new oil and gas projects. Investors are seeking greater transparency on how BP ensures these investments are disciplined and capable of generating acceptable returns.

In our view, BP’s response, as set out in its Notice of Meeting,[3] does not address the core issues raised in the resolution. BP:

BP provided updated guidance at the February 2025 Capital Markets Update that upstream capital expenditure from 2025-27 will increase from the previous guidance of $8.5bn to $10bn per annum. For investors, the key question is whether capital is being deployed in projects that are competitive, resilient and capable of generating acceptable returns.

Resolution 24 seeks disclosure that would allow investors to assess this. The information requested is reasonable, decision-useful and consistent with disclosures already provided by some industry peers.

(a) How does BP assess the relative cost-competitiveness of new projects?

BP states that it has a “top-tier oil and gas business in attractive basins”[9] but has not provided disclosure enabling investors to assess this. This information is highly material, as ACCR's previous research shows that the company’s gas assets are, on average, more expensive than 76% of global pre-FID supply; and its oil assets are, on average, more expensive than 53% of global pre-FID supply.[10] Similar analysis is already provided by peers such as Total.[11]

(b) How does BP account for cost overruns and delays in project schedules?

BP highlights that seven major projects started up in 2025, including five reportedly ahead of schedule. However, existing disclosures do not indicate whether these projects were delivered on budget or how project execution risks are incorporated into investment decisions.

In addition, these disclosures only cover projects started in 2025. ACCR’s analysis of BP disclosures since 2015 indicates that over 60% of BP projects with disclosed target start-up dates since that time were delivered later than planned.[12]

Disclosures made in BP's 2025 Annual Report suggest the company already has in place the processes and data required to meet the asks of the resolution and understands its investments’ sensitivity to cost and schedule slips. This suggests that it would not be overly burdensome for the company to provide the requested disclosures or require extensive new internal processes.

(c) How does continued exploration capex create value for BP’s shareholders?

BP’s existing disclosures provide information about exploration activities (e.g. new discoveries, exploration capex). The resolution seeks disclosure around how BP assesses the expected value of its planned exploration.

BP points to 12 exploration discoveries in 2025, including its largest discovery in 25 years. However, this does not explain how BP ensures that continued exploration capex creates value for shareholders.

This remains a highly material question for BP’s shareholders, as the company’s conventional exploration has become less successful, more expensive and less productive over time.[13] The company’s spending on exploration was 20% higher than the annual average for this decade.[14]

BP's response to resolution 24 – detailed ACCR view

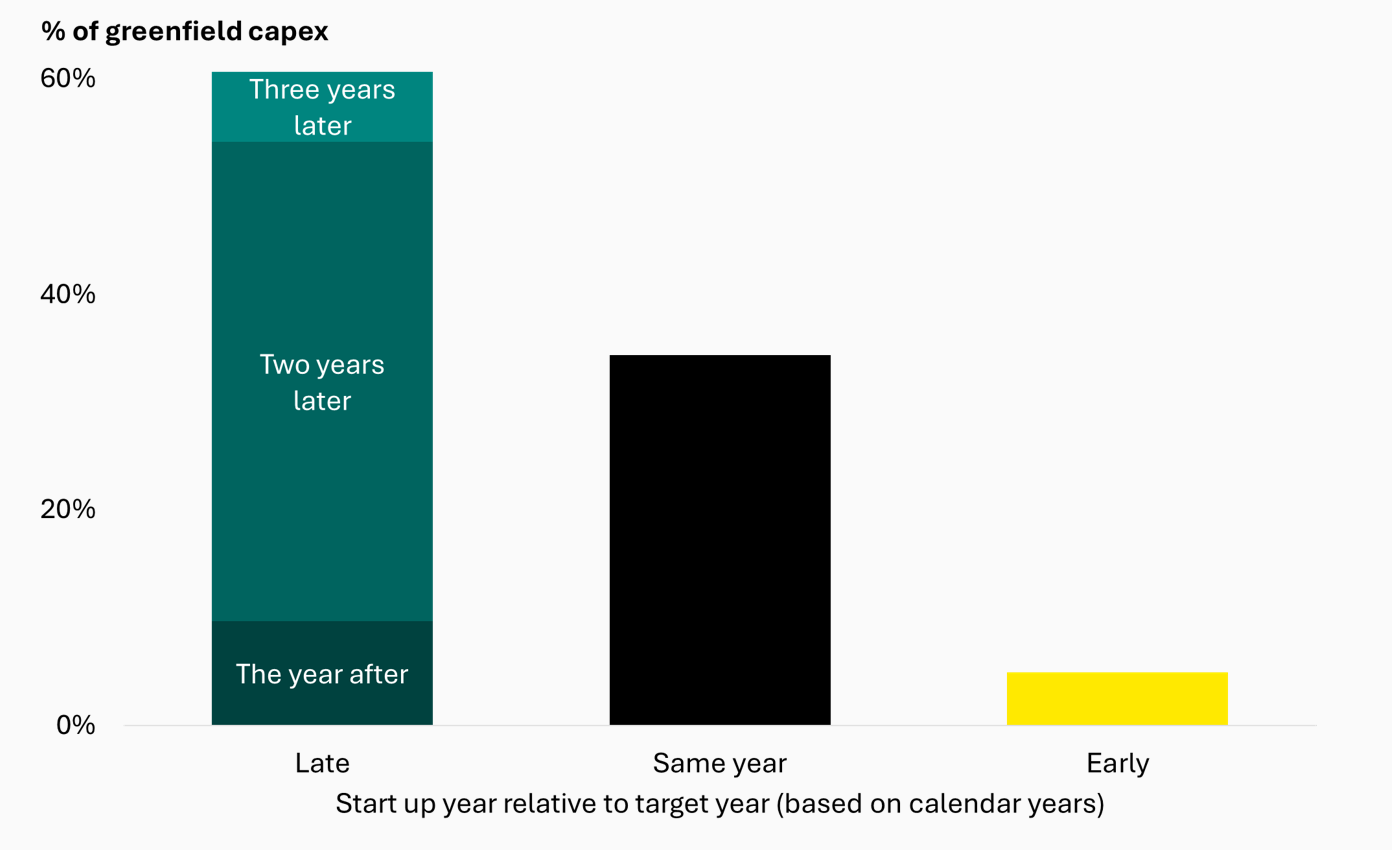

61% of BP’s projects with a disclosed target start-up date were late

Of the projects that reached FID, started up before the end of 2025, and disclosed a target start-up date, 61% started up late.[15]

For most of the projects, BP does not disclose a budget.

Of BP’s seven “major projects”[16] that started up in 2025:

We have not identified a BP-disclosed budget for any of these projects.

We identified 36 of BP's projects, of which 21 have a disclosed expected start-up year and came online by end-2025. These 21 projects represent approximately 63% of BP's total approved greenfield capex between 2015 and 2024. The remaining capex generally falls outside of BP’s consolidated reporting or was acquired post-FID.

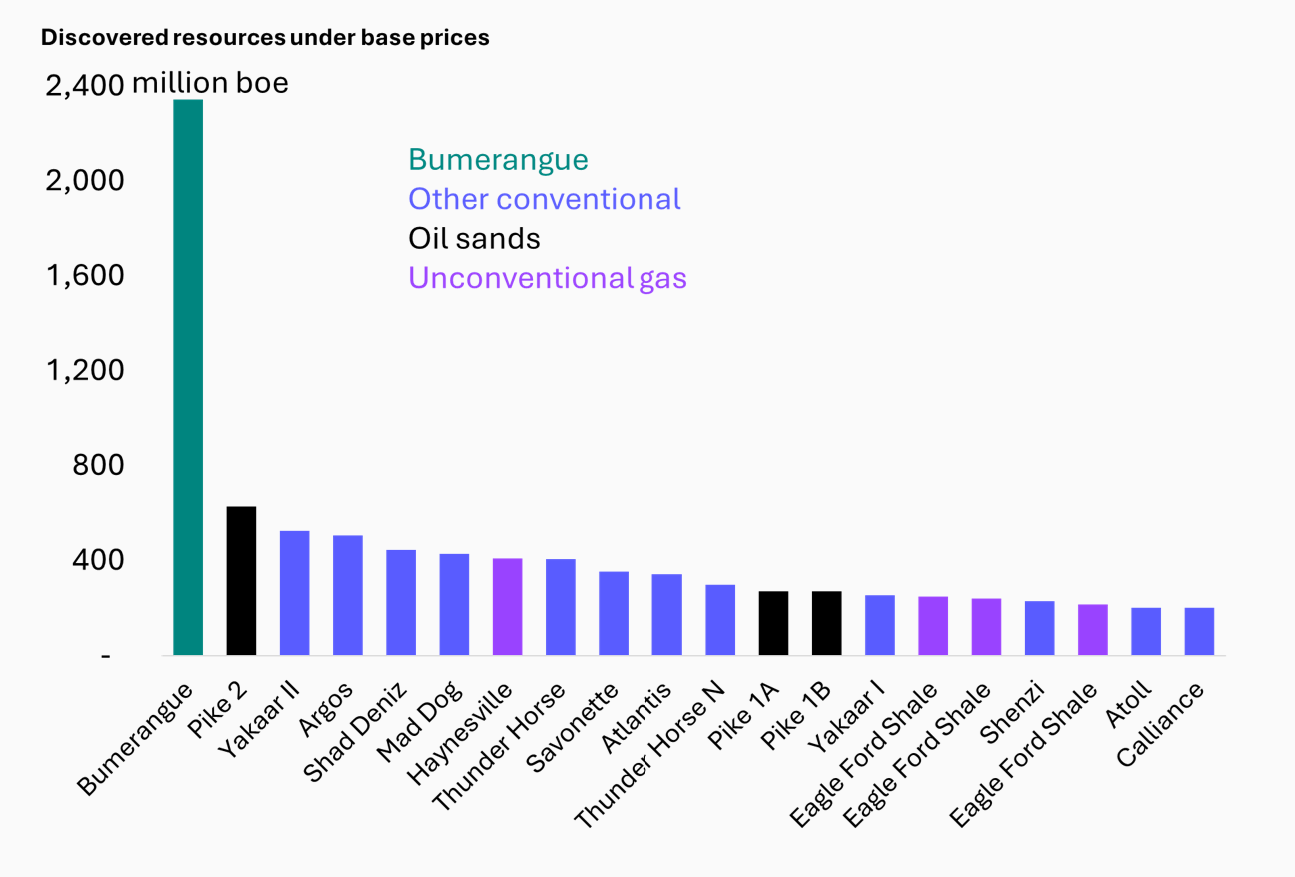

BP’s Bumerangue may not deliver material shareholder value

BP discovered Bumerangue in 2025 – its discovery largest in 25 years.

Based on Rystad Energy data – which is likely to be updated as BP discloses additional appraisal information – Bumerangue will generate[17]:

Bumerangue (Phase 1 and 2) has a higher break-even price than 81% of global pre-FID oil supply that could reach FID by 2035.

On average, BP has spent $1.3 billion on exploration each year this decade.[18] Under a forward price deck, this discovery could therefore fund BP’s exploration costs for about 8 months.

BP, “Appendix 3: Resolution 24,” in Notice of bp Annual General Meeting 2026, (Self-published, 2026), p. 23, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-agm-notice-of-meeting-2026.pdf. ↩︎

“Shareholder Resolution to BP plc on Upstream Capital Expenditure Disclosures,” ACCR, published Feb 3, 2026, https://www.accr.org.au/posts/shareholder-resolution-to-bp-plc-on-upstream-capital-expenditure-disclosures/. ↩︎

BP, “Appendix 3: Resolution 24,” in Notice of bp Annual General Meeting 2026, (Self-published, 2026), p. 23, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-agm-notice-of-meeting-2026.pdf. ↩︎

Ibid. ↩︎

BP, Capital Markets Update: February 2025, (Self-published, 2025), pp. 15-16 & 23-24, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-cmd-2025-presentation-slides.pdf. ↩︎

BP, “Appendix 3: Resolution 24,” in Notice of bp Annual General Meeting 2026, (Self-published, 2026), p. 23, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-agm-notice-of-meeting-2026.pdf. ↩︎

ACCR, Moving BP from rhetoric to action on capital discipline, (Self-published, 2025), p. 6, https://www.accr.org.au/downloads/accr_bp_rhetorictoaction_capitaldiscipline_261125.pdf. ↩︎

BP, “Appendix 3: Resolution 24,” in Notice of bp Annual General Meeting 2026, (Self-published, 2026), p. 23, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-agm-notice-of-meeting-2026.pdf. ↩︎

BP, bp Annual Report and Form 20-F 2025, (Self-published, 2026), p. 12, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-annual-report-and-form-20f-2025.pdf. ↩︎

ACCR, Moving BP from rhetoric to action on capital discipline, (Self-published, 2025), p. 14, https://www.accr.org.au/downloads/accr_bp_rhetorictoaction_capitaldiscipline_261125.pdf. ↩︎

TotalEnergies, 2024 Strategy & Outlook, (Self-published, 2024), pp. 23 & 30, https://totalenergies.com/sites/g/files/nytnzq121/files/documents/totalenergies_2024-strategy-and-outlook-presentation_2024_en_pdf.pdf. ↩︎

Percentage is based on share of greenfield capex. ↩︎

ACCR, Moving BP from rhetoric to action on capital discipline, (Self-published, 2025), p. 12, https://www.accr.org.au/downloads/accr_bp_rhetorictoaction_capitaldiscipline_261125.pdf. ↩︎

ACCR analysis of BP, bp Annual Report and Form 20-F 2025, (Self-published, 2026), pp. 242-247, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-annual-report-and-form-20f-2025.pdf; BP, bp Annual Report and Form 20-F 2023, (Self-published, 2024), pp. 250-253, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-annual-report-and-form-20f-2023.pdf; BP, bp Annual Report and Form 20-F 2021, (Self-published, 2022), pp. 257-258, https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-annual-report-and-form-20f-2021.pdf. ↩︎

The disclosures considered are BP’s annual reports 2015-2024; percentages refer to greenfield capex of the project portfolio, as per Rystad Energy data. ↩︎

BP, “Energy delivered: One year, seven big projects,” Energy in focus magazine, 14 January 2026. https://www.bp.com/en/global/corporate/news-and-insights/energy-in-focus/one-year-six-big-projects.html. ↩︎

NPV incorporates all cash flows from 2026 and a 12.2% discount rate that accounts for country risk. Forward price deck has a $58/bbl Brent price, or $69/bbl under Rystad’s base deck (RT25; simple average from 2026-2050). Capex is present value terms using the same base year and discount rate as for the NPV calculation. Inputs and calculations as of 10 March 2026. ↩︎

ACCR analysis of Rystad Energy data. ↩︎

Get email updates about new ACCR research and shareholder advocacy on specific topics of interest to you.

Sign Up