26th June 2026

Stay Informed

Get email updates about new ACCR research and shareholder advocacy on specific topics of interest to you.

Sign UpThis communication is for informational purposes only and does not constitute financial, legal, or professional advice. ACCR does not hold an Australian Financial Services Licence and does not provide financial product advice. The purpose of this communication is not to provide financial product advice. Please read the terms and conditions attached to the use of this site.

Investors have a critical window to influence business decisions that could align the steel sector with global climate targets.

New research in Nature Climate Change explains the potential scale and impact of carbon lock-in for the steel sector, and considers how targeted, near-term investment decisions can help prevent this.

The steel sector is responsible for around 7% of global CO2 emissions. Existing capacity of long-lived Blast Furnace-Basic Oxygen Furnace (BF-BOF) assets already creates substantial emissions lock-in, and investment decisions to extend existing assets or build new ones risks lock-in into the 2060s. By shifting capital away from coal-based steelmaking, especially in emerging markets, steel sector investment can drive significant climate mitigation.

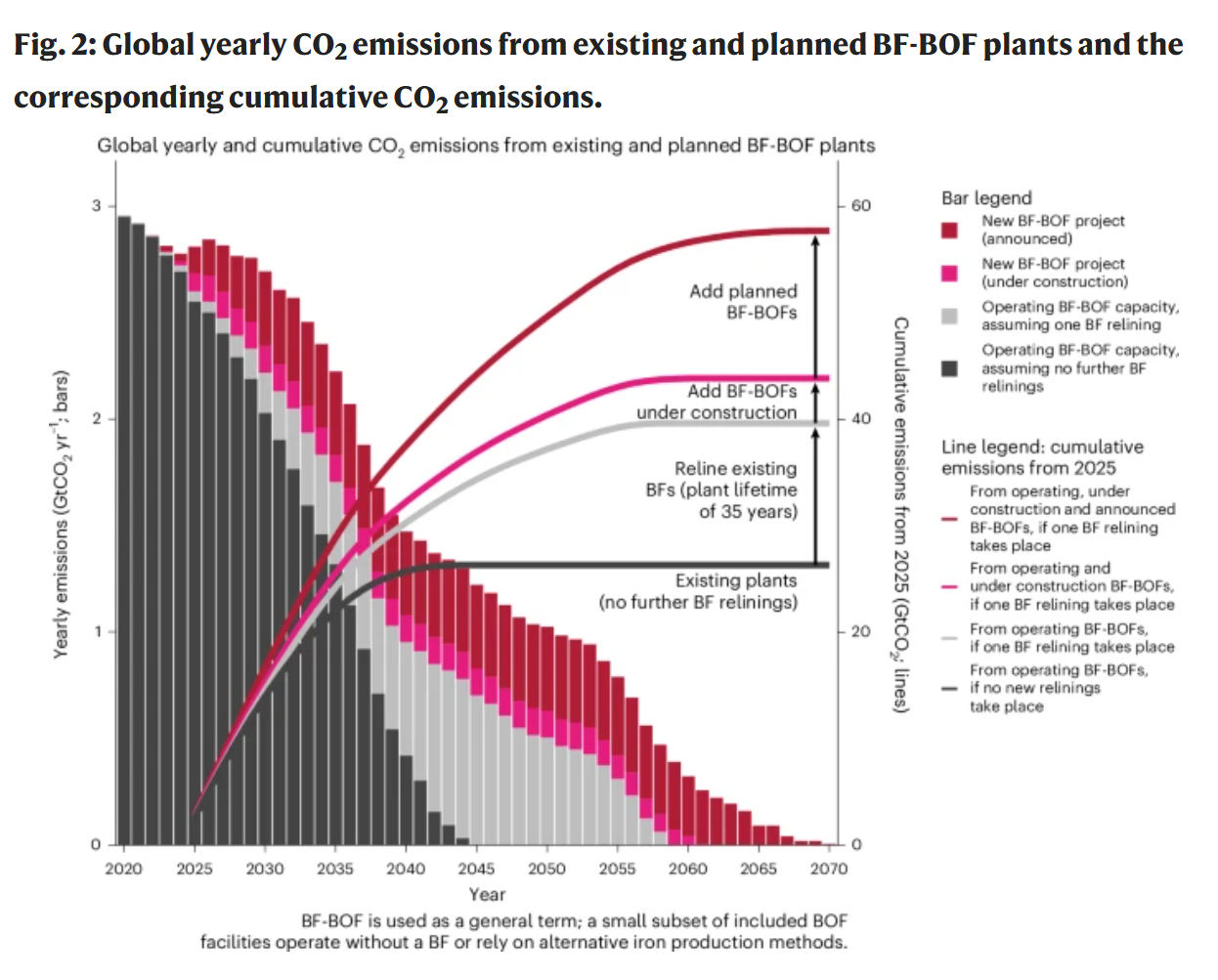

Investments in new coal-based steelmaking capacity, both announced and under construction, could add 19 Gt of cumulative CO2 emissions by 2070. This lock-in, when combined with the future emissions of existing assets, will produce a total of 58 GtCO2 by 2070.

If investments in coal-based steel capacity go ahead and these trends continue, the steel sector risks consuming 20% of the remaining carbon budget (114 GtCO2) for limiting warming to 1.7 °C.

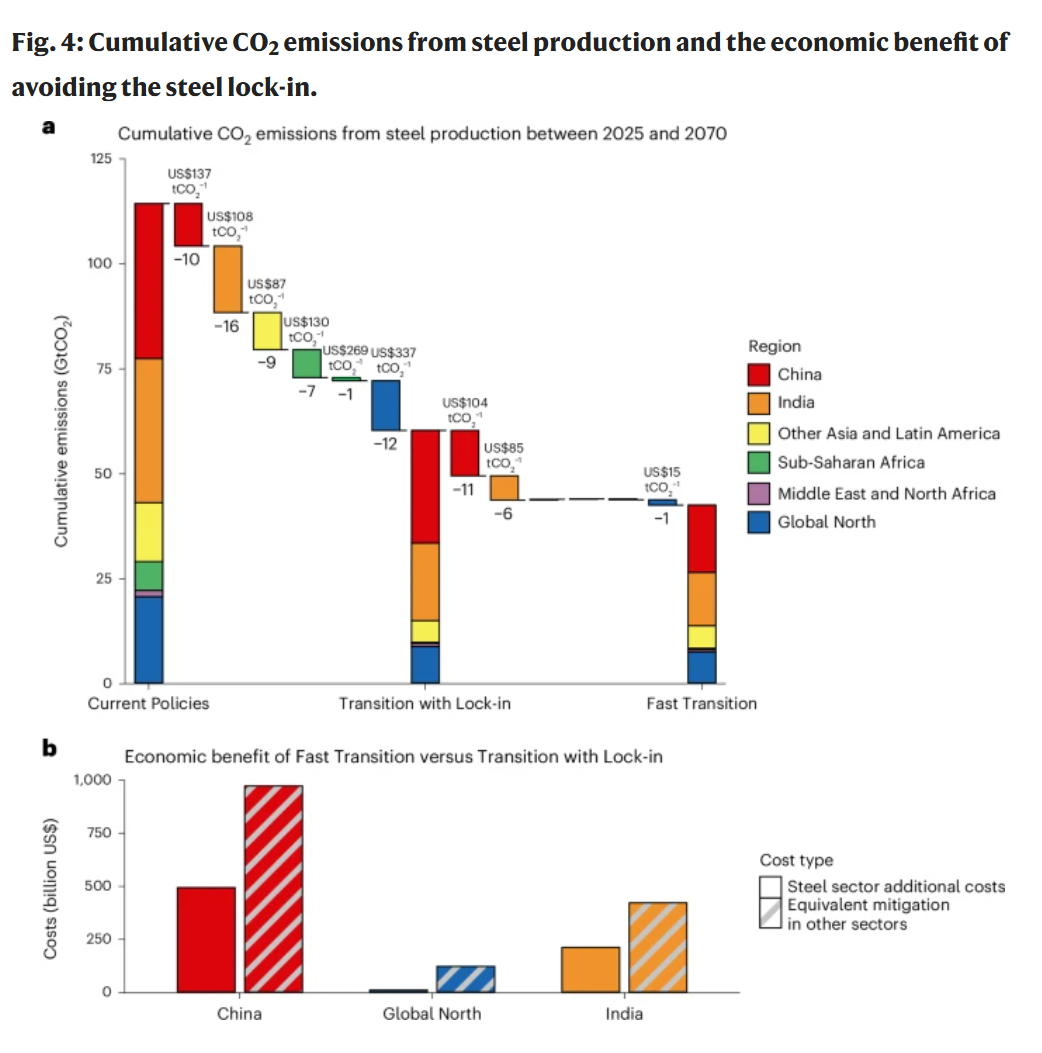

Avoiding further coal-based investment limits emissions lock-in and reduces costs. Deeper steel sector decarbonisation can be achieved at a lower cost per ton of CO2 abated. 60% of lock-in risk can be avoided at average abatement costs of US$100–150 per tonne of CO2.

There is still time to change course, as most new capacity is at the announcement stage, not the construction stage. Near-term investment decisions, especially in emerging markets, are critical. For example, 22 GtCO2 of emissions could be avoided in India alone by redirecting US$50 billion of climate finance to hydrogen-ready direct reduction steel plants before 2030.

Source: Figure 2, Averting the steel carbon lock-in through strategic green investments. (Methods - Steel plant data analysis)

These insights emphasise the critical opportunity investors have to influence near-term investment decisions and avoid decades of carbon lock-in. Investors in the steel sector can prioritise:

Source: Figure 4, Averting the steel carbon lock-in through strategic green investments. N.B. average abatement costs for CO2 emissions reductions achieved in each region are labelled above each segment.

ACCR supports investors globally to take effective action to mitigate the portfolio and systemic risks of climate change. For more information about our steel value chain work, please contact us.

Reference:

Bachorz, C., Dürrwächter, J., Gong, C.C. et al., “Averting the steel carbon lock-in through strategic green investments,” Nature Climate Change 16 (2026): pp. 681–689, https://doi.org/10.1038/s41558-026-02635-8.

Figures 2 and 4 from the above article are licensed for use under CC by 4.0.