Overview

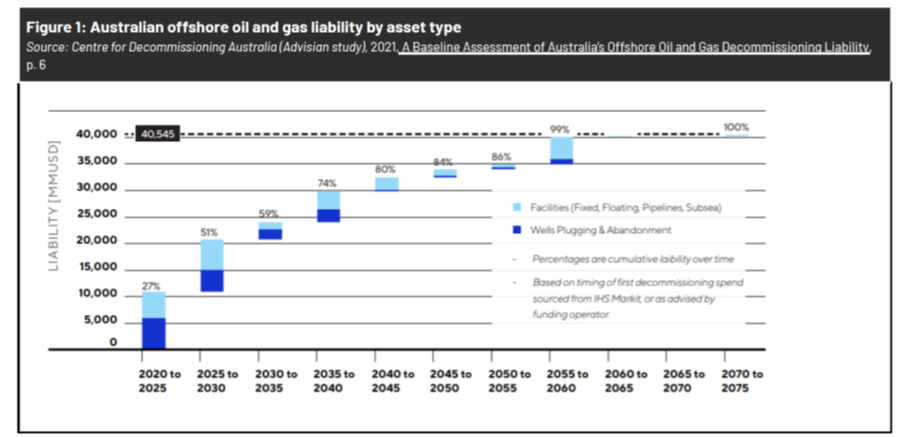

As Australia’s offshore petroleum industry sector matures, decommissioning obligations are increasing. Decommissioning is a significant liability for the industry going forward with the Australian government Department of Industry, Innovation and Science (DISER) estimating a substantial number of the approximately 136 fixed facilities (including pipelines) likely to commence decommissioning activities in the coming decade. National Energy Resources Australia (NERA) forecast decommissioning costs over the next 50 years for the nationwide offshore oil and gas industry to be USD$40.5 billion, with almost half this work to occur in the North Carnarvon basin off the coast of Western Australia (see Appendix 1 & 2). The Australian regulator (NOPSEMA) expects the decommissioning to be ‘complex, expensive, span many years and introduce many new and significant safety, environmental and well integrity risks’.

Key findings / analysis

A multitude of decommissioning risks is creating uncertainty around operators' plans and final costs. Inexperience, uncertain timelines and costs, environmental and social license risks, regulatory scrutiny and energy transition pressures are all factors affecting Australian companies' decommissioning plans and estimated costs

- Inexperience: Decommissioning necessitates skills and equipment that vary from standard construction activities, and Australia's decommissioning industry is still in its infancy with concerns around the possibility of a lack of technical expertise. To date, there has been very little decommissioning of infrastructure in Australian Commonwealth waters.

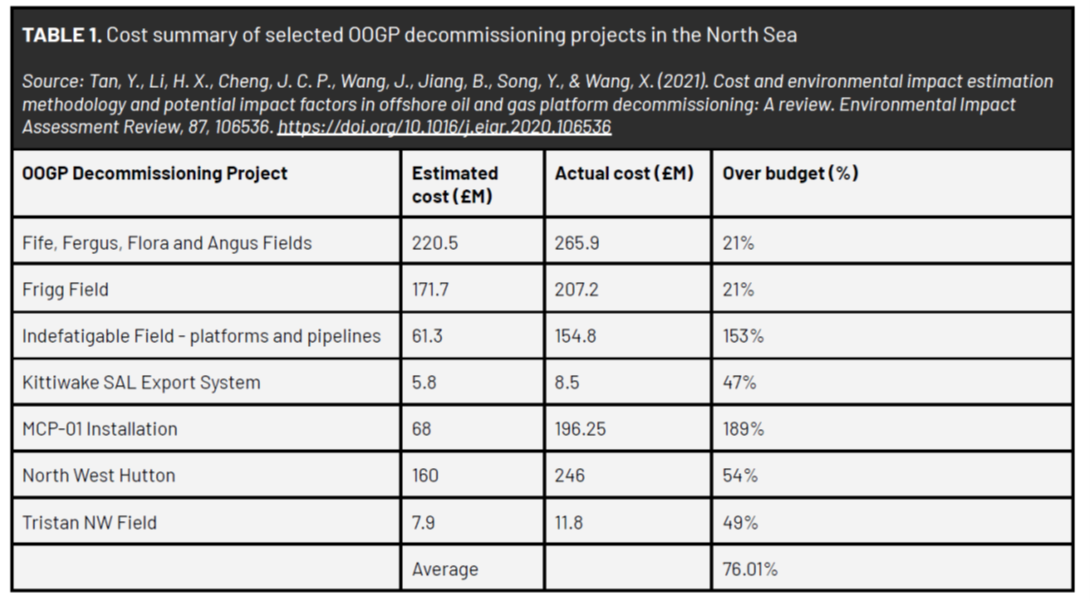

- Decommissioning has a global history of cost overruns: Research indicates there has often been a big discrepancy between the estimated and actual decommissioning costs of offshore oil and gas platforms. Recent analysis of selected offshore oil and gas platform decommissioning projects in the North Sea found that the average actual cost was about 76% greater than estimated cost (see Appendix 3).

- Environmental Risk: Recent Environmental Improvement Notices indicate some offshore Australian operations are posing serious threats to the environment due to oil and gas leakage, including as a result of operator failures. There are limited studies exploring the ecological impacts of decommissioned oil and gas structures. A recent study of 43 marine decommissioned wells in the Central North Sea found that gas release from decommissioned hydrocarbon wells is a major source of methane there and concluded that the large number of hydrocarbon wells in the North Sea 'likely constitute a major source of methane'.

- Repurposing equipment risks: The repurposing of offshore pipelines, wells and facilities may be an attractive option for deferring or avoiding decommissioning expenditure (e.g., for offshore wind projects, offshore carbon capture and storage, rigs to reef). However, repurposing is not a guaranteed solution for all offshore infrastructure due to technical and safety barriers. For example, the North Sea Transition Authority has developed a screening tool and determined that opportunities for repurposing platform topsides, jackets and subsea systems for decarbonisation projects are likely to be limited.

- Energy Transition Risk: The challenge of decommissioning is occurring in the context of decarbonisation and energy transition pressures, which as suggested by the Australian Accounting Standards Board may increase provisions for decommissioning due to regulatory changes or shortened project lives.

Regulatory scrutiny has tightened and the legislative framework has changed significantly. The national legislative and regulatory framework for decommissioning has changed significantly in Australia over the past 5 years, and operators are now dealing with several new limitations. There is a risk that oil and gas companies operating in Australia have not reflected this in their decommissioning assumptions.

- NOPSEMA becoming more assertive: In response to a Ministerial directive, which asked the regulator to heighten its oversight of decommissioning obligations, NOPSEMA has introduced a suite of decommissioning policies, including a maintenance and removal of property policy and a 5-year Decommissioning Compliance Strategy and Plan. NOPSEMA now requires all structures, equipment and property to be decommissioned to approved end-state within 5 years of permanently ceasing production and all wells to be plugged within 3 years of permanently ceasing production and removed after another two. Companies have until 2023 to lodge a formal plan outlining how they intend to do this.

- Legislative changes following the Northern Endeavour/Northern Oil & Gas Australia (NOGA) liquidation case makes it more difficult to divest the decommissioning liability. Following the liquidation of NOGA, the task of decommissioning - and a hefty bill to cover costs - was initially passed by default to Australian taxpayers. Government inquiries followed, leading to the introduction of an industry levy to cover cleanup costs, expected to raise $3.4billion over a decade. Trailing Liability provisions were also introduced which are designed to ensure that the costs and liabilities associated with decommissioning will be borne by the petroleum industry. The provisions do this by allowing the government, if required, to call back former titleholders to undertake remedial work.

- Recent ASIC investigation on Woodside: In 2021, the Australian Securities and Investments Commission (ASIC) highlighted asset values and provisions as key areas of regulatory focus. In February 2022 ASIC revealed following ongoing investigations into Woodside Petroleum Ltd.’s reporting of restoration provisions for offshore infrastructure assets, that Woodside had provided an additional $239 million for restoration costs on future decommissioning and improved its disclosures of the basis for providing for future restoration costs.

Shareholders need more information about how liabilities are being measured and managed.

Currently,

- Scope of the task unclear: It is difficult to obtain a comprehensive picture of the number, age and stage of Australian operators' offshore assets, based on annual reporting documents. While the Federal government urges titleholders to keep, and regularly review, an inventory of infrastructure in their title areas, companies do not self-publish such inventories. Although regulators expect decommissioning to be planned for and managed proactively, throughout a project's life, shareholders are often not privy to these plans until the company has begun or is very nearly about to begin works.

- Timelines are uncertain: The Australian offshore oil and gas decommissioning liability has been estimated at $US40.5 billion to 2050, with a significant portion of work due to occur between 2020 and 2030. However, the state and cost for many ageing offshore oil and gas facilities in Australia is uncertain - existing public datasets are limited, and company disclosure is generally minimal. Currently, Environmental Plans (EP) are not required to be put to the public for comment. In effect, shareholders of Australian listed companies often have a limited view of company plans for decommissioning in the short and medium term.

- Removal plans are unclear: Many operators are assuming that they will be able to leave a significant amount of infrastructure 'in-situ', despite the fact that the full removal of offshore infrastructure is currently expected in Australia (although deviations may be pursued in circumstances and if regulatory approvals are granted). Regulator NOPSEMA has questioned if operators are properly valuing offshore assets on the basis of full removal. Liabilities are being calculated on this basis - i.e., the ability of companies to leave at least some of their infrastructure at sea underpins company restoration provisions. For example, Woodside has stated that if it was required to remove 'all, or a substantial portion of' its infrastructure, its provisioning would increase by $300-$500 million, plus extra costs which have not been assessed or calculated

Questions for management

In ACCR's view, it is in investors' interests to seek to understand the following:

- All major assumptions underpinning a company's decommissioning estimates, in particular those regarding:

a. The ability to leave offshore infrastructure 'in-situ', noting that regulatory approval to do so is required;

b. The timing of decommissioning works, noting that the regulator now requires infrastructure to be decommissioned to approved end-state within 5 years of permanently ceasing production (and all wells to be plugged within 3 years);

c. The level of planning in place, and whether this is commensurate with the scale of decommissioning required;

d. Where companies have plans to repurpose facilities, such as for carbon capture and storage (CCS) or offshore wind, further detail on the technical viability and the probability of regulator approval, along with how these plans influence the costs and timing of decommissioning activities.

Different infrastructure removal options - for instance, leaving in-situ, partial removal or full removal and disposal - will carry different risks and costs. These should be disclosed. If a company is reliant on gaining regulatory approval to leave infrastructure at sea, it should also disclose the additional cost if this approval is not granted.

- How firm these assumptions are, and if they are consistent with current regulatory guidelines.

- The age and stage of Australian offshore assets, and the cost/timing of decommissioning (especially within JVs - this will allow investors to analyse whether consistent assumptions are applied across the industry).

- How a company's current decommissioning costs are represented in, or can be reconciled with, recent industry-wide estimates (i.e., those published by NERA of US$40.5bn).

- Sensitivities to the timeline of decommissioning/restoration around the useful life of assets using different oil and gas demand scenarios, including the IEA Net Zero by 2050 scenario.

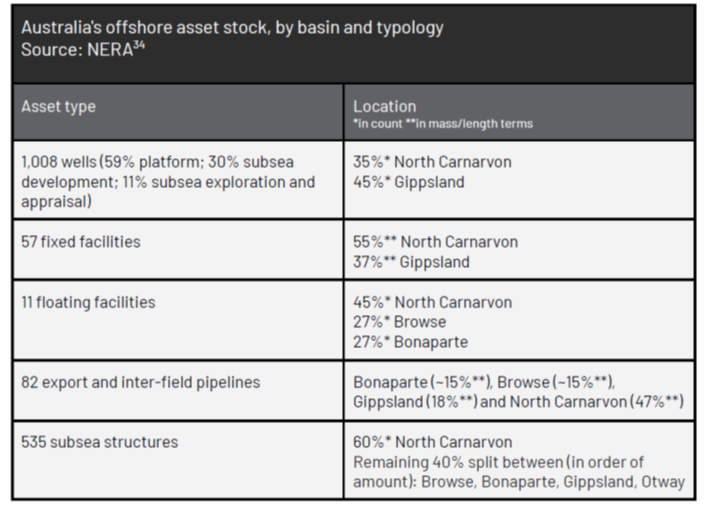

Appendix.(1)

Appendix.(2)

Appendix.(3)

Download this summary or our full analysis.

Please read the terms and conditions attached to the use of this site.